Back

Featured

Tax

8 mins

The Tax Benefits of SyntheticFi Securities-Backed Loans

Learn about the tax advantages of SyntheticFi's lending solutions over traditional securities-backed loans, including universal tax deductibility against capital gains.

Joseph Wang

Key Takeaways

Traditional Securities-Backed Loans (e.g. TriState SBLOC or Schwab’s Pledged Asset Line) | SyntheticFi Loans | |

|---|---|---|

Tax Deductibility | Interest deductible only when used to buy taxable investments (e.g. stocks, bonds), up to net investment income. | Interest always deductible as a capital loss (60% long-term, 40% short-term), regardless of loan purpose. |

Ineligible Uses | Non-deductible for personal expenses (e.g. car, home) or tax-exempt securities (e.g. municipal bonds). | No restrictions; deductible even for personal expenses. |

Deduction Limits | Capped at net investment income (e.g. dividends, short-term gains); excess can be carried forward. | Deductible against capital gains or up to $3,000 annual income, with carry forward. |

Tax Filing | Requires itemized deductions, Form 4952; limited under AMT. | Doesn't require itemized deductions. Reported via 1099 from custodians; supported by major tax software. |

Example | $500K loan, $25K interest, $7K investment income: saves $2,240 (32% tax bracket). | $500K loan, $25K interest: saves $9,400 (20% long-term, 32% short-term tax rates). |

Traditional Securities-Backed Loans - Tax Deductible Only When Buying Investments

The deductibility of interest on a traditional loan—whether it’s backed by securities or any other form of collateral—hinges on how the borrower uses the funds. If the loan is used to purchase taxable investments, then the IRS permits deducting the interest paid on the loan from investment income. This is categorized under the investment interest expense deduction. There is a cap on the deduction, however. The borrower can only deduct up to the amount of the total income generated from investments.

Suppose Tony has borrowed $500K on margin to purchase more stocks and bonds, effectively leveraging up his portfolio. During the tax year, Tony pays $25K in interest, and his portfolio generates a total of $7K in dividends. In this case, Tony can deduct the $25K interest paid on the loan, paying no tax on the $7K of investment income. If Tony' s income is taxed at a rate of 32%, he saves $7K × 0.32 = $2,240 on his taxes. But the remaining $18K of unused interest can't be claimed as a deduction elsewhere on his tax return, including ordinary income. (However, it can be carried forward into a future tax year.)

Ineligible Purchases

The IRS has rules designed to tie the deduction of interest on loans to taxable investment activities. So interest payments are not tax deductible in the following situations:

Personal expenses: If the loan proceeds are used for non-investment purposes, such as buying a car, paying a tax bill, purchasing a residence, or covering living expenses, the interest is not deductible. The IRS requires that the loan be used to acquire taxable investment property for the interest to qualify as an investment interest expense. Deductions are typically allowed for expenses related to generating taxable income but personal expenses are seen as consumption, not income-producing, so they don’t get a tax break.

Tax-exempt or tax-preferential investments: If the loan is used to buy or hold tax-exempt securities, like municipal bonds—or generate income given preferential tax treatment like qualified dividends—then that the interest is not deductible. This restriction ensures that deductions align with taxable income generation, preventing taxpayers from claiming deductions on income that isn’t taxed.

Exceeds net investment income (in the current year): As discussed, the interest is only deductible up to the amount of the net investment income (e.g. dividends, interest, short-term capital gains) for that tax year. Any excess interest isn’t deductible in the current year, though it can be carried forward to future years.

Qualifying investment interest expenses

When filing taxes, there’s no field asking, "Was this loan used for investments?" Instead, the IRS relies on the borrower's compliance with rules outlined in IRS Publication 550, Investment Income and Expenses. The borrower is implicitly certifying the interest qualifies by claiming it. If challenged, records would be needed to show the funds went toward taxable investments, not personal use.

If Tony borrowed the $500K via a securities-backed loan, spent it on a car, but made $6K in dividend income from other stocks, he can’t deduct the loan interest against that $6K because the loan wasn’t used for investment purposes, which affords no tax savings.

It is a risky move to claim investment interest expense deduction when loans are not used for investment purposes. IRS employs a tracing rule (detailed in Publication 550 and Topic No. 505, Interest Expense) to determine deductibility. This means they look at where the loan money went. Claiming it against unrelated investment income is a common misunderstanding, but it’s not how the law works. If claimed anyway, the IRS could audit the filer, request proof of use, and disallow the deduction, adding penalties or interest on unpaid taxes.

Limited to Deductions Against Investment Income

The investment interest expense deduction allows the borrower to deduct the interest payments only on their investment income—in non-retirement investment accounts—which is subject to income tax rates. Specifically, it applies to interest, ordinary dividends, short-term capital gains, annuities and royalties. It does not apply to returns that are taxed at capital gains rates, such as long-term stock sales, qualified dividends (which receive preferential tax treatment so aren't considered investment income), nor does it apply to business or passive income.

In the same tax year, if Tony had long-term capital gains of $30K and qualified dividends of $20K, Tony still wouldn't be able to claim the $19K of remaining interest as a deduction.

Requires Itemized Deductions, Constraint under AMT

As a final note, the borrower must itemize their tax return in order to take advantage of the investment interest expense deduction, as opposed to taking the standard deduction.

To claim the investment interest deduction, the client must file Form 4952, Investment Interest Expense Deduction, and determine which part of the interest paid is deductible. The client must complete two versions of the Form 4952: one with regular itemized deductions and one under Alternative Minimum Tax (AMT) calculations instructed under Form 6251, where investment interest is not deductible. The client needs to file the Form 4952 with higher taxes.

It's probably best to work with a tax professional to help you file this on your tax return and make sure that it's done correctly to maximize your savings.

Universal Tax Deductibility of Interest From SyntheticFi Loans

SyntheticFi uses a strategy involving box spreads on S&P 500 (SPX) Index Options, so that interest expenses on loans procured through our platform can be claimed as a capital loss, as opposed to just an investment expense against investment income, like traditional securities-backed loans. This way, the interest is always tax-deductible, regardless of how the loan proceeds are used.

How It Works: Section 1256 Contracts

S&P 500 (SPX) Index Options, the building blocks behind our lending program, are considered Section 1256 contracts. These contracts are marked-to-market at the end of every year, which means contract owners can claim a loss on these contracts even if the contract is still outstanding. So when clients borrow money through our program, they will receive the principal when opening the trade, and pay the principal plus interest at settlement time. However, each year the loan is unpaid, they will incur a loss equal to the interest expense. So these losses can be written off each as capital losses—a mix of 60% long-term and 40% short-term.

If Tony borrowed $500K against his portfolio through SyntheticFi to purchase a car, while incurring $25K in interest by the end of the year, he can deduct $25K × 60% = $15K from his long-term capital gains and $25K × 40% = $10K from his income (short-term capital gains is taxed at income rates). At a long-term capital gains tax rate of 20% and an income tax rate of 32%, Tony potentially saves $15K × 0.2 + $10K × 0.32 = $9.4K in taxes.

Fixed Interest Loans - Balloon Interest Payment, but Annual Deductions

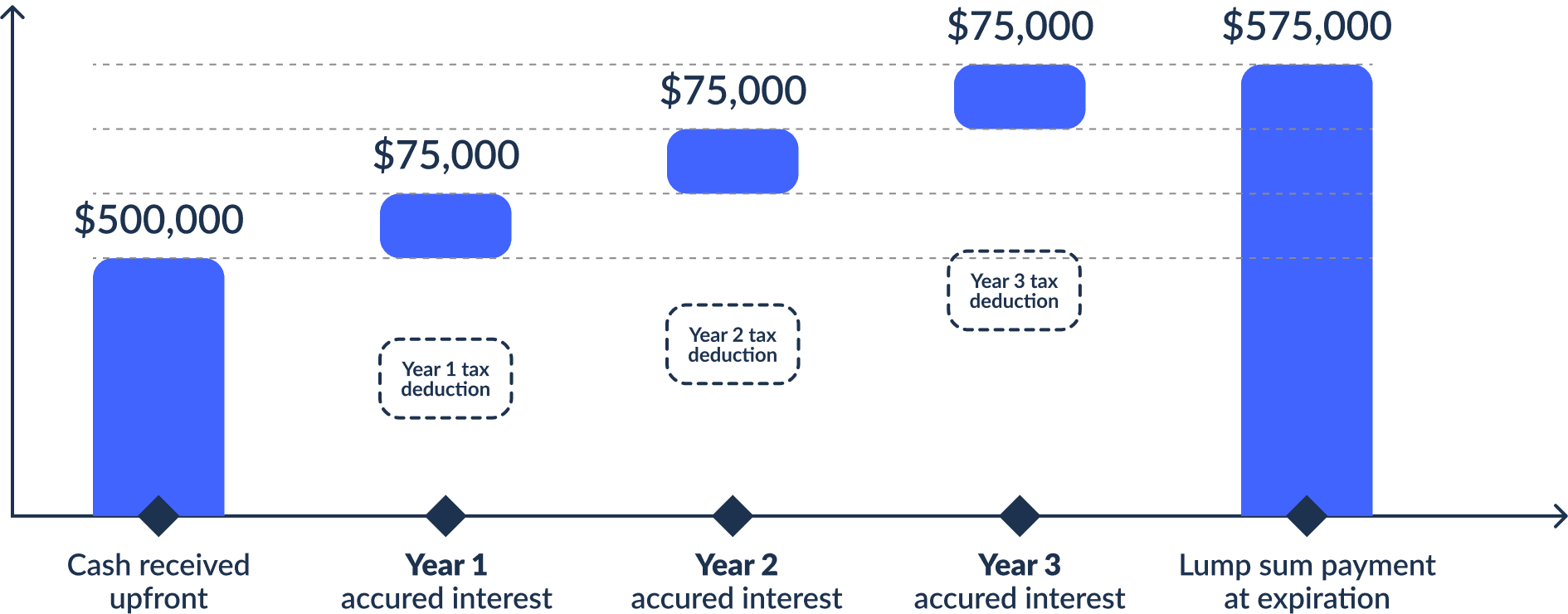

SyntheticFi clients can elect for a fixed interest rate loan with a box spread contract that lasts for up to 5 years. In this case, the interest is not paid until the term of the loan has ended (i.e. the underlying Section 1256 contracts expire). These clients will still claim a capital loss each year: for tax purposes, custodians will use the fair market value of the loan to calculate the losses on those contracts at the end of each year, which will equal the accrued interest for that year.

If Tony elected to borrow the $500K at an annual fixed rate of 5% for a 3-year term, then after the end of the first year, the mark-to-market value of his loan will likely be $525K ($500K + 5%). $15K (60% of $25K) will be treated as a long-term capital loss and $10K (40% of $25K) will be treated as a short-term capital loss (i.e. income deduction).

At the end of the loan period, Tony would make a lump sum repayment of $575,000. But for the final tax year, Tony would only claim $25,000 in capital losses (60% long-term and 40% short-term).

What if there are no capital gains to offset the losses? If the borrower's capital losses exceed the capital gains, the IRS allows filers to deduct up to $3K against their income in a given tax year. Any excess losses after $3K can be carried forward to future tax years indefinitely. In subsequent years, the filer can again deduct up to $3K annually against ordinary income (after offsetting any new capital gains) until the loss is fully used.

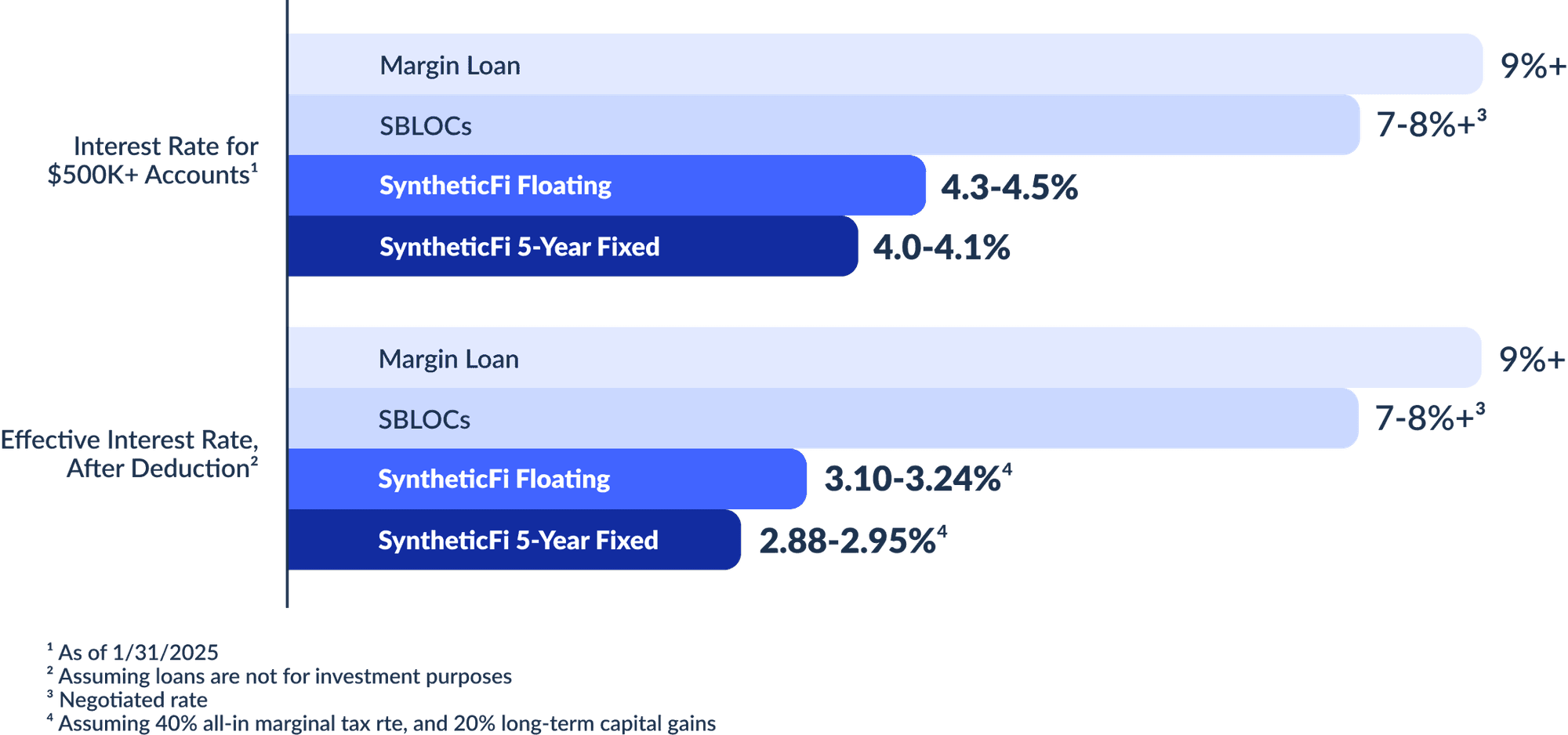

Effective interest rate

Since the interest expenses on a SyntheticFi loan is always tax-deductible, regardless of use, we offer superior effective interest rates on funds borrowed with our strategy (after deduction):

(The 0.5% management fee to SyntheticFi is not tax-deductible.)

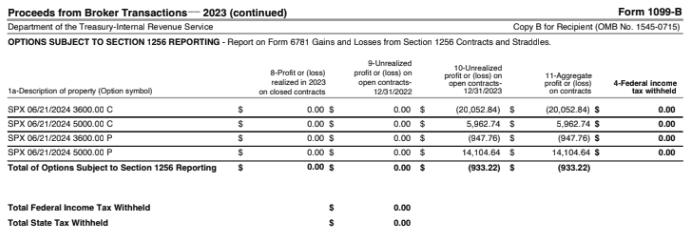

Tax reporting

Custodians such as Schwab and Fidelity will report the gains and losses on Section 1256 contracts as part of the consolidated 1099 package. Read more from Schwab.

Reporting for gains and losses on Section 1256 contracts are supported by major tax reporting software, such as TurboTax, and can be easily handled by a professional tax preparer.

Conclusion

The tax implications of traditional securities-backed loans depend on their purpose, with interest deductibility limited to taxable investment activities, leaving personal uses ineligible. SyntheticFi’s innovative approach, leveraging S&P 500 (SPX) Index Options and Section 1256 contracts, ensures interest is always tax-deductible as a capital loss—60% long-term and 40% short-term—regardless of how the funds are used, offering flexibility, attractive interest rates, and potentially higher tax savings. As with any financial decision, consulting a tax professional is crucial to maximize benefits and ensure compliance with IRS rules and regulations.